If you Opt-in Old Tax Regime then you can get the Tax Exemptions. Important for tax planning. It reduces the tax burden of an assessee. Let’s take a look at important deductions in Income tax F.Y. 2020-21 and A.Y. 2021-22. Or if you Opt-in as New Tax Regime, then you can not avail the below all Exemptions.

INCOME TAX DEDUCTIONS F.Y. 2020-21 & A.Y. 2021-22

FOR INDIVIDUAL & HUF

| Section | Deduction Limit | Investments / Expenses |

80C | Up to Rs. 150,000/- In (80C, 80CCC & 80CCD(1) together) | Life Insurance Premium P.P.F.(Public Provident Fund) Investment E.P.F. (Employee’s Provident Fund) N.S.C. (National Savings Certificate) Investment & Accrued Interest ELSS Mutual Funds (Equity Linked Saving Schemes) Five years Bank or Post Office Tax Saving Deposits S.C.S.S (Post Office Senior Citizen Savings Scheme) Principal repayment of Home Loan Kid’s Tuition Fees Sukanya Samriddhi Account Deposit scheme |

80CCC | Contribution to the annuity plan of L.I.C. or any other Life Insurance Company for receiving a pension from the fund is considered for tax benefit. | |

80CCD(1) | Allowed to an Individual who makes deposits to his/her Pension account (like e NPS). Maximum deduction allowed is 10% of salary (in case of the taxpayer being an employee) or 10% of gross total income (in case of the taxpayer being self-employed). | |

80CCD(1b) | Additional deductionUp to Rs. 50,000/- | The amount deposited by a taxpayer to their NPS account. Contributions to Atal Pension Yojana are also eligible. |

| 80D | Up to Rs. 25,000/- &Rs. 50,000/- for Senior citizens | Mediclaim / Health Insurance Premium |

80EE | Up to Rs. 50,000/- | Home Buyers can claim an additional Tax deduction of up to Rs 50,000 on home loan interest payments. The below criteria has to be met for claiming tax deduction under section 80EE. The home loan should have been sanctioned in FY 2016-17. Loan amount should be less than Rs 35 Lakh. The value of the house should not be more than Rs 50 Lakh & The home buyer should not have any other existing residential house in his name. |

80G | 100% (generally in case of government funds) or 50% (generally in case of non-governmental funds) | Contributions made to certain relief funds and charitable institutions. This deduction can only be claimed when the contribution has been made via cheque or draft or in cash. But deduction is not allowed for donations made in cash exceeding Rs 10,000. In-kind contributions such as food material, clothes, medicines etc do not qualify for deduction under section 80G. |

80TTA | Up to Rs. 10,000/- | Interest on deposits in SAVINGS BANK ACCOUNT, co-operative society or post office can be claimed under this section. Section 80TTA deduction is not available on the interest income from fixed deposits. |

Other Rebates:

24(b) | Up to Rs. 200,000/- in case of self-occupied property or no maximum limit if the property is let out | Interest on housing loan is allowable as deduction on accrual basis not on paid basis (even if account books are kept on a cash basis) if capital is borrowed for the purpose of the purchase, construction, repair, renewal or reconstruction of the house property. The deduction can be claimed for two or more housing loans. |

87A | Up to Rs. 2500/- | This rebate is available on tax on total income to a resident individual if his total income does not exceed Rs. 350,000/- |

Withal Income Tax Exemptions are available under Sec.10 and other deduction withal of Income Tax Act, 1961.

• Leave Peregrinate Allowance under clause 5 of Section 10(5).

• House Rent Allowance under Section 10(13A).

• Allowances to MPs/MLAs under section 10(17).

• Allowances for the income of minor u/s 10(32) etc.

• Standard deduction of Rs 50,000 u/s 16.

• Deductions from House Property Income of interest paid on house loan (Self-occupied/Vacant) u/s 24.

• Regalement allowance and employment/ professional tax will not be available.

• Deduction of Rs 15,000 for family pension u/s 57.

• Set off of carrying forward loss and depreciation from earlier assessment years is not sanctioned.

• Without setting off a loss under the head income from house property.

• Without the benefit of expedited depreciation u/s 32(1)(iia). However mundane depreciation can be claimed u/s 32.

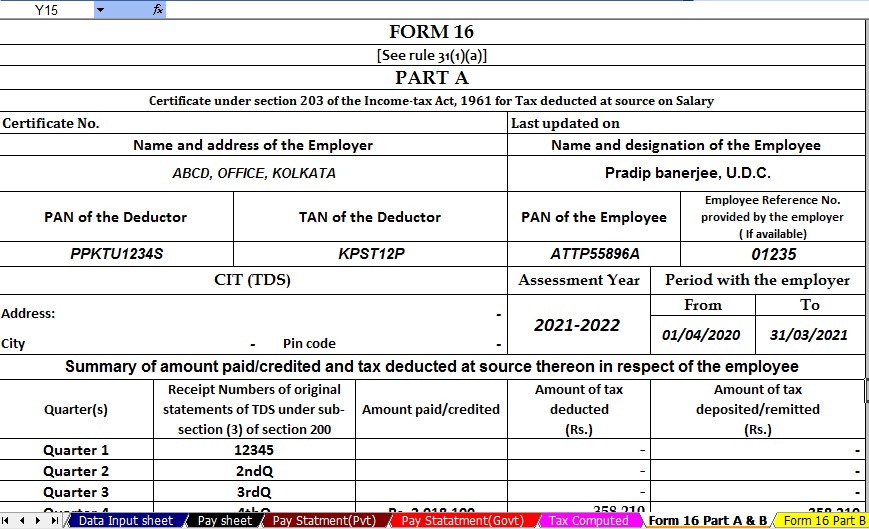

Automated Income TaxPreparation Excel Based All in One for Govt and Non-Govt Employees forF.Y.2020-21 (Old Tax Regime and New Tax Regime U/s 115BAC)

[This Excel Utility can prepare at a time your Tax Computed Sheet + Individual Salary The structure as per the Govt & Non-Govt Concern’s Salary Pattern + Automated Arrears Relief Calculator U/s 89(1) with Form 10E + Automated Income Tax Revised Form 16 Part A&B and Form 16 Part B as per Budget 2020]